Do You Feel Lucky?

The Emotionally Intelligent Investor - Part III

I was sick to my stomach when I went home that evening. I realized I had blown it and that the market was about to crash.

- Stanley Druckenmiller (October 18th, 1987)

Preface

This is the third and final post in a series regarding The Emotionally Intelligent Investor by Ravee Mehta. This post will deal with intuition.

Most Important Things:

The market may appear random, but many patterns repeat over and over again. Intuition is forged by way of recognizing these patterns.

Good decision-making should leverage intuition, while also being safeguarded with logic.

Experience does not necessarily lead to expertise. Expertise is developed through a focus on process, not outcome. Thus, intuition is best built through an objective review of prior decision-making processes.

Instead of simply listing risk factors, try to visualize failure and then work backward to understand patterns that help with sensing danger.

“When done correctly, investing not only leads to wealth, but also to being a better human being.”

Contents

Patterns

Not checkers

Relentless review

Danger

Life

Patterns

Turning to intuition, Mehta argues that it is built upon extensive exposure to patterns and that it finds expression in our visceral emotions:

Intuition is a feeling that is generated from pattern recognition. When we build expertise in a field, we are not just accumulating information. Experts develop mental maps so that certain patterns come to be expected. Their expertise becomes so ingrained that they may not understand how or why things seem to make sense. They just do. When events happen that seem consistent with prior patterns, an expert’s emotional brain centers generate positive feelings. When something happens that violates the expected pattern, they produce negative emotional responses.

Ultimately, this culminates in a form of tacit expertise:

In The Social Animal, David Brooks states, “The result is that the expert doesn’t think more about a subject, she thinks less. She doesn’t have to compute the effects of a range of possibilities. Because she has domain expertise, she anticipates how things will fit together.”

What’s noteworthy is that the ideal deliberative process of the expert contrasts sharply with that of the novice:

Novices, on the other hand, actually do better when they depend more on an analytic framework to make decisions. This is because novices have not yet built up enough necessary expertise. Their gut instincts are less well-informed. Novices use their intellect to decide between many options. Babies learn language and how to walk by carefully selecting each word and thinking about each step. Teenagers learning to drive, actively think about how much pressure to apply to the breaks when going into a sharp turn. Experts intuitively choose a single option and then use their intellect to decide if it is a correct choice.

Not checkers

Nonetheless, Mehta is fully aware of the dangers of relegating one’s System 2 thinking entirely to the sidelines:

Like chess grandmasters, investors who have built adequate expertise should employ gut instincts. Not doing so would ignore years of experience and training. However, these intuitions should be safeguarded with logic. In The Power of Intuition, Gary Klein states, “We don’t want to rely entirely on impulses. Impulses and intuition have to be balanced with deliberate, rational analysis. But rational analysis can never substitute for intuition.”

Mehta then goes on to outline how he practically employs these guard rails when evaluating an investment opportunity:

For example, when someone pitches me an investment in a sector in which I have no experience, I automatically know to proceed cautiously. I have identified certain patterns that tend to recur over and over again and I try to stick with investments that fit those patterns. Whenever I have a gut feeling regarding a specific investment, I almost habitually try to remind myself of a similar prior fact set. If the potential investment does not remind me of any pattern I have seen successfully work before, I pass on the investment and move on. If after understanding the company’s fundamentals, I cannot come up with risk / reward characteristics that make sense, I move on. If after talking to another investor, it becomes apparent that there are too many major differences between the current situation and the pattern I thought the investment fit into, I move on.

Not only does this mode of operation dovetail precisely with Buffett’s well-known admonition for investors to operate within their circle of competence, but it also appears to find correspondence with the habits of chess grandmasters:

This is a somewhat similar process to how a chess grandmaster may dismiss his initial gut feeling. After careful analysis, he realizes that his initial gut feeling is not safe. However, the chess grandmaster still utilizes his intuition to come up with another possible move to evaluate. He follows this process over and over again until he comes up with a move that he intuitively feels good about and appears logically acceptable. Like the best investors, great chess players are those who have built up enough pattern recognition / expertise / intuition to point them in the direction of the best possible moves. They make sure the game is played so that their competencies are best utilized. They also have a good analytical process for making sure their gut instincts are safe. Finally, they maintain mental flexibility. Great chess players may decide to retreat from an attack or realize that they are being overly defensive. Similarly, great investors often reverse their positions after they realize they are wrong or after their trip wires are triggered.

Relentless review

How then to build the necessary expertise to buttress our burgeoning intuition? Mehta again turns to chess to furnish an answer:

…the secret to success in chess and in most other endeavors is a relentless review of prior decisions and focused practice on areas that require improvement. Critiquing prior decisions develops intuition, because it increases the odds that prior patterns stick somewhere in one’s mind. The result is that next time a similar problem is presented, the good chess player either has higher confidence in making the correct move again or has improved his intuition so that it points him towards the better move.

However, Mehta is also aware that investing is not entirely analogous to the beautiful board game:

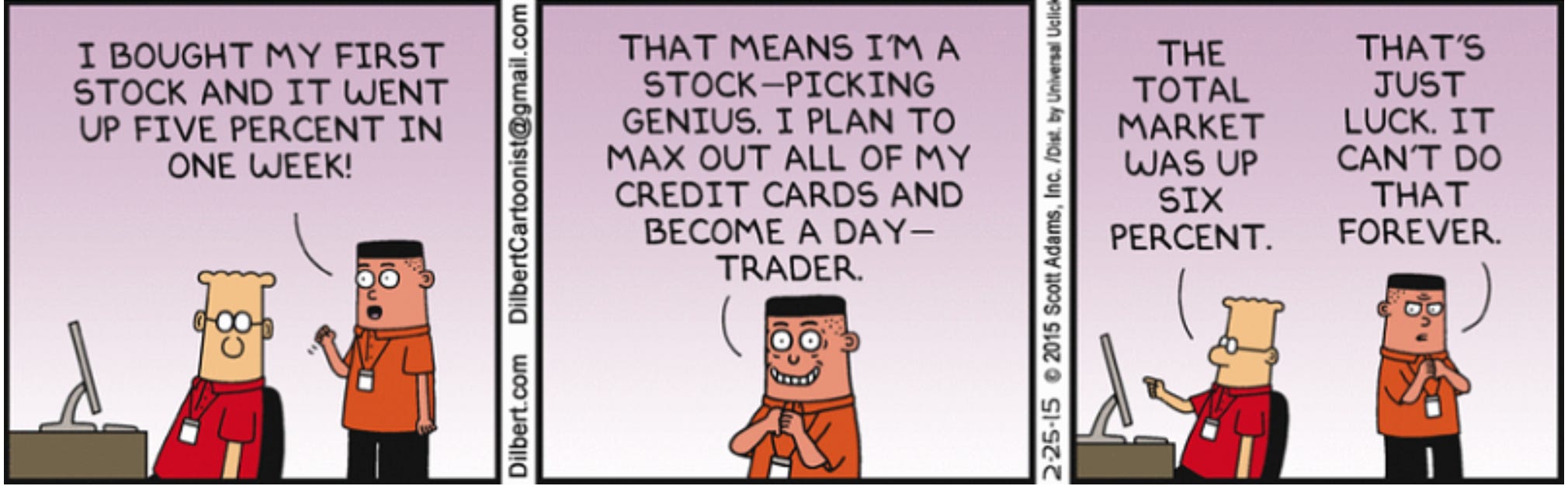

There are a couple of important characteristics that are unique to investing. This is where the chess analogy breaks down. First, randomness plays a much larger role with investing. Second, investing intuitions become obsolete over time. It is because of these differences that very few investors appear to have good intuition over the long term.

To counter randomness precluding the development of intuition, Mehta provides the following advice:

It is important to remember that expertise is developed through the review of the decision-making process rather than outcomes. When evaluating an investment decision, it is important to try to take into account random variables…This is why I began this book discussing self-awareness. Only someone self-aware will admit when luck bails them out of making a bad decision. It is important to focus on patterns that seem to occur over and over again within the overall market…However, what is most important is that one is honest with oneself with respect to the role of luck. Only then can one actually learn from a prior decision.

Likewise with the risk of one’s hard-fought intuition no longer sufficing:

Obsolescence is another reason why intuition needs to be safeguarded with logic…The only solution to obsolescence is constant evolution. The best firms are those that foster a culture of intuition building. They maintain flexibility to change their approach to where new opportunities lie. Investors like Martha should not become complacent with a certain expertise. They need to try to constantly build new intuitions.

Danger

Their intuition having been established, Mehta provides some striking examples of how the greats would attune themselves to its dictates:

For some great investors, intuition built to sense danger is actualized into physical changes. George Soros learned to recognize that something was wrong with his portfolio whenever acute back pain set in. Other investors, as exemplified by the quote from Stanley Druckenmiller at the start of this chapter, feel sick when they start to realize they are in trouble. These investors are self-aware enough to recognize that negative emotions, or their physical manifestations, such as back pain or an upset stomach, are signals. When something starts to happen that is contrary to your investment thesis or that you previously contemplated during a pre-mortem exercise, your brain produces a negative emotional response which sometimes is expressed physically. Dismissing these feelings is a mistake. Instead, investors should learn to recognize these emotions as alarm bells. I am not implying that people should just reverse course every time they have a bad feeling. Rather, bad feelings should be catalysts to logically reevaluate one’s positioning. Remember: investment decisions should start with gut feelings, but should always be safeguarded with logic. Most of us are biased towards overconfidence. Visualizing failure can offset this basic human inclination.

Visualizing failure is a key component of Mehta’s investing practice, one that he has instituted primarily as a means to manage risk and avoid catastrophic loss:

It is common practice for analysts to list risk factors associated with their investments, but few investors actually try to visualize failure. A pre-mortem exercise involves mental simulation of failure and then thinking of all the possible reasons for its occurrence. This may sound the same as quickly listing risk factors, but it is very different. When you mentally simulate your investment failing, you actually try to feel the pain from the loss on the investment.

The upshot is that this repeated exposure to the visceral experience of failure acts as a type of cognitive buffer when things - inevitably - fall apart:

Investors that have a better idea of what can go wrong with their investments are more in control. This empowers them to sell when others are still evaluating the unexpected development or are inappropriately adding even more risk. Moreover, I hope that these simulations will aid me to quickly recognize buying opportunities such as when traders become overly concerned about certain industry noise that does not fundamentally impact the company’s earnings power or growth prospects.

I constantly conduct visualization exercises in which I envisage my net worth declining past my threshold amount. I work backward to think of scenarios that could cause this to happen. I then adjust my portfolio to minimize risks. Very often, these adjustments also limit the potential upside of my portfolio, but that is a tradeoff I am willing to make given my own personal motivations…Nevertheless, I will still believe I made the right decision, because it will have allowed me to sleep at night.

Life

Mehta memorably concludes with some of the broader implications of seeking to develop and implement self-awareness, empathy, and intuition:

What does this all mean for life outside of investing? The successful investor needs to stay humble, introspective and empathetic so as to continue being good at what he or she does. When done correctly, investing not only leads to wealth, but also to being a better human being. This book’s concepts are applicable to many aspects of life. Being honest with oneself and making an action plan to deal with vulnerabilities can only be helpful. For example, while I am relatively outgoing, I sometimes still feel anxiety in certain social situations. Conducting visualization exercises before these types of events helps me to feel more prepared and in control. Before social gatherings, I sometimes try to think about what I can learn from each of the people I will meet. Events that once caused me anxiety are now get-togethers I increasingly look forward to. They are opportunities to learn. Moreover, improved social awareness only leads to more fulfilling relationships with family and friends. Finally, even professional investors make many more non-investing decisions than trading choices every day. Objectively reviewing these decisions can only help build the intuition to make the correct future judgments that lead to being a better parent, spouse, neighbor, boss, etc.

Note: I hope you’ve enjoyed this series of posts on The Emotionally Intelligent Investor. As a reminder, you should absolutely buy, read, and reflect upon the book for yourself.