The Passion of Chamath Palihapitiya - Part III

Work

As we would wish that a painter who is to draw a beautiful face, in which there is yet some imperfection, should neither wholly leave out, nor yet too pointedly express what is defective, because this would deform it, and that spoil the resemblance; so since it is hard, or indeed perhaps impossible, to show the life of a man wholly free from blemish, in all that is excellent we must follow truth exactly, and give it fully; any lapses or faults that occur, through human passions or political necessities, we may regard rather as the shortcomings of some particular virtue, than as the natural effects of vice; and may be content without introducing them, curiously and officiously, into our narrative, if it be but out of tenderness to the weakness of nature, which has never succeeded in producing any human character so perfect in virtue as to be pure from all admixture and open to no criticism.

- Plutarch, Cimon

Preface

This is the third and final post attempting to explicate, in his own words, Chamath Palihapitiya’s approach to markets and decision-making.

Disclaimer

The following post is fashioned from Chamath Palihapitiya's public statements, interviews, annual letters, and blog posts. Sources are cited. Despite every attempt having been made to preserve their original intent, errors and misinterpretations are, of course, possible. Caveat lector.

Contents

Markets

SPACs

Heat

Venture

Correlation

Founders

Hiring

Sources & Footnotes

1. Markets

If you want a simple high-level summary of how the market works, it’s somewhat analogous to a train. Sometimes the train is going up a hill, sometimes it's going down a hill, and sometimes it's going off a cliff.1 Moreover, it's important to observe how the train’s boxcars are arranged. The boxcar at the front are computer trading algorithms, which really dictate the early momentum, shape, and volatility of the market. Next, are hard money long-only institutions and hedge funds; humans that are running money. Then, at the back of the train, is retail. [1]

Over time, if you follow the positioning of CTAs and hedge funds, you can sort of see where markets go. If you take that set of information and you do a join with where the volatility index is, you get a decent directional sense of what's going to happen. This is not advice, and you should research this for yourself, but if you actually backtest it, there’s some truth to it. [1]

For example, in Q1 of 2023, hedge funds had very little exposure. The CTAs had largely been short prior and thereafter been forced to cover into a rally. The VIX was decaying as volatility was leaving the market. When you put these things together, typically markets go up. When that happens, then the train flips into reverse. Retail runs in, then hedge funds will become a little overexposed, and CTAs will become net long. Thereafter, maybe something happens in the world which triggers volatility to rise, and then we reverse the cycle. [1]

2. SPACs

SPACs are short bursts of effort from a fundraising perspective, while VC fundraising requires more hand-holding. As a head of a VC fund, you are no longer an investor; you become the head of investor relations. This is not a job I either liked or wanted to do. [2]

I think SPACs are here to stay, and I think that that’s a good thing. Historically, we only had one way for companies to raise capital, which was via a traditional IPO. Then, we had direct listings. Looking ahead, I think SPACs are going to be a really important tool in the arsenal of entrepreneurs. [3]

Let me take a step back and explain why. During the prior cycle, VCs did a massive disservice to entrepreneurs by telling them that they should never go public. Why was this the wrong advice? At some point, when you have a nominal amount of scale, the key to winning is your cost of capital. When you have product-market fit, you want as many dollars as you can get your hands on to invest in scaling, with the least amount of dilution and overhang to your balance sheet. So, being public is something that should actually be pulled forward in the life cycle of a company. [4]

That's how Silicon Valley used to work in the 1990s. Companies used to go public when they were at a two, three, or four hundred million dollar market cap. People forget that Amazon, Google, and Microsoft collectively only raised $125 million before they went public. They were not waiting for some moment of perfection. By being public, they could explain their business to people with very different expectations on rates of return. When you sell to a public market investor, their alternative is to buy a 10-year bond that today yields 4%, so 10% looks amazing to them, 15% looks outrageous, and 20% looks illegal. Whereas the opposite is true for private investors. If you're not growing by 100% you're “failing”, but that's not really failing. [4]

In year seven of the prior cycle, it was clear to me that Social Capital needed to be a net seller of equities in the market. I couldn't keep waiting with billions of dollars of imputed value in our book when none of it was liquid. That was insane to me. So, when I learned about SPACs, I thought, “This is a very clever tool,” because it helps companies that are really capital-intensive. Now, SPACs, like IPOs, have had good outcomes and bad outcomes.2 Some entrepreneurs who are doing very hard things will find SPACs a means of raising money in the least dilutive way possible. Those entrepreneurs running a software business with 90% gross margins may decide a $50 million IPO is enough. To each their own, but the optionality should be there, because it will give entrepreneurs the ability to negotiate against the financial infrastructure, lead to less dilution, and ultimately give founders more power. In the fullness of time, that is better. [4]

However, I think we need to build trust and credibility. In my opinion, the best way to do that is to have more regulation and transparency in the market. I think that there are too many SPAC sponsors, and I think we could do a lot more to provide signals on sponsor quality, and deal quality. As the capital markets mature, you’ll have more banks competing to bring these companies public. I think sponsors will become fewer, but there’ll be higher quality in general. [3]

Right now, I think the most disruptive idea is for someone to go and raise a $250 million SPAC, where $249 million of it is their money, and a million of it is from a number of other investors, just so they qualify for the SEC's rules. Then, when they go to a company, they’re able to say, "The money is guaranteed. Here's a $250 million IPO. Let's agree on a price, you and me, that's fair. Let's negotiate executive compensation, let's negotiate the dilution package for the executives, let's negotiate how much other money you may need from other people," and it’s done. Now, you need to be well-capitalized to do that, but I do think that that's a powerful idea. [4]

3. Heat

I'll give you a paint by numbers approach for how to build a multi-billion dollar venture organization. Step one, you need to have a brand, which can come in two ways. If you were running an organization in the seventies, eighties, and nineties, you’ve already built your brand. This would be the Sequoias and Kleiners of the world. They benefited from having high-quality deal flow and very few competitors, so the odds of funding a Larry Ellison or a Steve Jobs was high. [5]

Now, 30 years later, the industry is completely different, so you’ll need to find another way of building a brand. That other way is by manufacturing ‘heat’. When I started Social Capital, I replicated the growth practices I utilised at Facebook and built an entire process around that inside of the organization. Alongside that, to be honest, I was a little immature. I said things that were a little crazy, but it created heat.3 Now, a decade later, I would say I’ve matured because that only works when you're younger. People love young dilettantes, but when you're 46, and you’ve got five kids, you’ve got to be boring and reliable. [5]

So step one is to build a great brand, and you’ll have to figure it out because nobody's going to give it to you. How many people have read Warren Buffett's letters? Unbelievable heat. There's only one thing I keep in my desk, which is two binders of all of his letters. Think about Paul Graham. He had to start building heat for himself at Y Combinator. How did he do it? With his essays. If you read those early Y Combinator essays, they're gold. Marc Andreessen, how does he build heat? Andreessen has an entire organization of 50 or 60 people whose sole job is to produce tons of content to get in front of you guys. David Sacks is a good friend of mine, how is David building heat? He's providing expertise in this one very specific area that he has, and he's trying to distinguish himself within it. The point is you have to find a way to create heat. Have something interesting to say. If you don't, get around people who have interesting things to say so that you can work with them. [5]

Step two is to learn the art of portfolio construction. Nobody thinks about this, but when the market are in a correction, how do you insulate yourself from losses? The way that you insulate yourself from losses is to avoid doing crazy high-priced rounds. The way to do that is by getting in front of a bunch of people who are starting companies at the earliest stages, assessing the founders, and funding them. Essentially, you’re just buying free options. Then, as things start to scale, you have to have the discipline to aggressively double down on your winners. Alongside this, you’ll need to partner with someone who is risk-averse, not risk on, whose entire upbringing makes them unbelievably afraid of ever losing money. When you're pounding the money in, they'll help scrutinize your decision-making, minimize your mistakes, and just make sure that you don't blow yourself. [5]

Put all these pieces together, and success should build on itself, like a flywheel. In time, you should have a pretty decent track record. Remember, anyone can do it, but step one is the key. If you get step one right, all the other steps are easy. [5]

4. Venture

I think much of what is said about the craft nature of venture capital is what Bezos refers to as a narrative fallacy. In the past, VCs were rewarded despite adopting a very imprecise methodology, by virtue of operating in a very small, nascent category. It was easy for VCs to believe their job was to run around with other people's money, take bets, and buy a bunch of free options. To be fair, that wasn't such a bad thing because that kind of behaviour was rewarded for a long time. It wasn't necessarily their fault. Now, the reality is that technology is omnipresent, and venture will be an asset class, no different from private equity. It'll become mature, it'll become scaled. There'll be platforms. As that happens, VCs are going to have to become more systematic. [5]

At a certain level, I think you can reduce a lot of the venture business down to just looking at the numbers. However, there are unique moments in a venture company's evolution that require judgement gleaned from experience that can't come from a computer.4 Computers are not good at understanding the J-curve dynamics of certain projects, where a two-pizza box project at Amazon, like Kindle or AWS, becomes a billion dollar juggernaut. I think those decisions are very difficult to assess and require reasoning that computers are not good at doing. There are nuanced trade-offs because, at the end of the day, the CEO of a portfolio company is still making bets and allocating capital. [5]

So, I think a more quantitative approach will be an important part of venture, no different from the public markets. There are some quant funds that do very well, but they do well in a niche. They do well in a kind of mechanic that's repeatable. Typically, the capital can't scale, and typically the capital can't go across strategies. I suspect that if you have an algorithmic form of venture investing, it'll be similar. [5]

If you're going to be an expert at this craft and be excellent, you have to be very technical. I'm the largest investor in my funds; I take it very personally. I'm hyper-competitive, and I only think about returns first. Everything else is a far distant second. It's not nearly as much fun as you may think because the easy job is to give the entrepreneur money. The hard job is to sell. The hard job is to sell it in secondary. The harder job is to find a landing in M&A when the thing doesn't work. The hard job is to force somebody to do a big reduction in force because they're running out of money. The hard job is to fire somebody because they've proven themselves to be incapable of running a business. It’s a very, very tough job to do well. [5]

5. Correlation

There’s an enormous amount of correlation among VCs in Silicon Valley; they’re all trafficking in the same stuff.5 I went into PitchBook and pulled the 400 deals we’ve done at Social Capital since the beginning of time – a bunch of big deals and a bunch of very small deals. Then I pulled all the PitchBook data for every other VC that you can name, and I asked my team a simple question: when we do a deal, how often are any of these folks doing it as well? A good sign is if I'm at zero, or as close to zero as possible. [4]

Why is that important? It’s important because when you see a drawdown, it's going to hit everybody except the ones that are uncorrelated. They will be in a position to write capital. Some firms’ correlation is off the charts – fifteen percent of their deals are just doing every deal Benchmark does, nine percent the same deals as what Sequoia does. It doesn’t mean they’re bad people, but they had a miscalculation, they confused alpha and beta. Alpha is when you’re uncorrelated. When correlated with everybody else and the market goes up, you go up: that’s beta. And that is really good when rates are zero and the market's ripping, but it's terrible when rates are not zero, and the market is not. [4]

It turns out, what you should do as an early-stage VC is the opposite of what late-stage folks should do. Late-stage folks should have close to 100% correlation. If you’re a Tiger or Coatue, of course, you should be picking from these deals. But if you’re early-stage, and you’re copying a bunch of other early-stage people, you’re just repeating the same risk over and over again. You need new risk to stay independent; otherwise, you’re not going to be in a position to write new checks. Correlation is also concentration. When you're diversified, you're better. [4]

So, I’m trafficking in things that are highly uncorrelated to the gestalt of Silicon Valley, which can be a lonely business. It's really valuable in moments where markets get crushed because correlation is the first thing that causes massive destruction of capital, but it requires a lot of thinking outside the box. It's lonely because you're taking risks, and you’re a public personality, so your mistakes aren't private. It's like being an athlete. If you really want to be a winner, you have to be able to hit the shot in front of the fans. If you miss it, you have to be willing to take the responsibility of the fact that you bricked it. These are razor-thin margins at the end of the day; all I can control is my preparation, and whether I'm in the best position to launch a reasonable shot. [5]

6. Founders

When I first meet people, I never ask to see a resumé. At the early stage, the only thing that matters is the psychology of the founders. I look for a couple of threads. One is the combination of ego and humility. Let’s be honest, a lot of CEOs are ego-driven people. But they also have to be humble in some very precise ways around ideas and decisions, and being able to change their mind. That’s an idiosyncratic combination. Another thread is intellectual curiosity. They ask a lot of “why” questions, and they’re comfortable with the ambiguous nature of things that are unknown. The last one is that you want somebody who’s ultra-resilient because there are just so many trials and tribulations to building a business. One day, it can feel like you’re on the top of the world, and the next day it’s all crumbling down. Can you compartmentalize it, put it in context, and enjoy it? [6]

I also couldn't care less about the business plan. Instead, I just try to take the time to let the founder reveal themselves. If you were ever raising capital, and you asked me, 'What do you think about this business?' I'd probably say eight to ten words for hours and just listen. I’m trying to build a sense of who this person is, unpack their biases, and identify where they might fail. Once I have a rough sense of that, which is not necessarily right but a starting point, then I can go and understand why this idea makes sense at this moment. [7]

By the way, if you go to a very good school, you'll get a lot of interview prep in a bunch of this other stuff. You can trick people into being a lot more resilient than you actually are because you learn the language of resiliency, and you can memorize it, and then you'll regurgitate it to the hiring manager at Google and Amazon, and they'll hire you. You have to be able to see past that, and you have to take people out of their comfort zone. That's all I care about. Is this person resilient? Are they psychologically capable of getting punched in the face and figuring it out? [5]

I’ve come to believe that the best leaders all have the same skill, which is that they are exceptional investors. Jeff Bezos is literally the single best investor of our generation. This guy has compounded capital at more than 40% a year over 20 years. And that is unheard of, but he's a CEO. If you go back and read his letters, basically Bezos has a very smart principle, which is he thinks in bets. The two pizza box team thing. How do you iterate, how do you find failure modes, and how do you get to success? [5]

7. Hiring

I've interviewed hundreds of people, so I've seen the aftermath of all of my bad decisions. I've had hundreds of reps of seeing my biases play out, and the things that I fall for have changed over time. When I was young, I had a huge bias for well-educated people, which is, I didn't like them. I would go out of my way to not hire them. I didn't like the credentials. I just assumed that they were great at playing the game, but that turned out to be wrong. I had a huge bias for very, very technical people, and that turned out to be wrong. You’ve just got to go through the reps. [5]

Starting a business, any kind of business, is really hard. Most people don't know what they're doing, and as a result, make enormous mistakes. With regards to hiring, this may be a little heterodoxical, but I think there are really only three kinds of mistakes. [7]

First, you'll hire somebody, and they're really, really average, but they're a really good person. Second, you'll hire somebody, and they weren't candid with who they actually are. Thirdly, you’ll hire somebody, and they're not that good morally, but they're highly performant. I think successful companies have figured out how to handle these three situations because these are often the factors, in my opinion, that determine success and failure of a venture.6 Keep, demote, promote, fire, what do you do? [7]

Personally, I believe that folks in bucket one are incredibly important and useful people. If a company is like a body, they are like cartilage. Can you replace cartilage? Yes, but would you if you didn't have to? No. A great example is if you go on YouTube and search for clips of how Kobe Bryant's teammates described how their behavior, not performance, changed by being somewhat closer to him. I think that's an important psychological thing to note for how you can do reasonably good team construction if you're lucky enough to find generational talents. You have to find a composition of a team that allows people to continue to add value. [7]

In terms of buckets two and three, if these people are senior and running an organization, I think the answer is to fire them. No matter how good you are as an organization, dishonesty and ethically compromised behavior will just inject poison into the company. [7]

Honestly, this is what I've learned over 11 and a half years. As an investor, if you’re willing to just keep chipping away, you'll eventually peel back enough of these layers, and you'll see it. [7]

8. Sources & Footnotes

Palihapitiya, Chamath. "Chamath Palihapitiya Interview: Wharton Private Equity and Venture Capital Club Fireside Chat Series.” Wharton PEVC Club, 2023.

Celarier, Michelle. "The Unusual Ambitions of Chamath Palihapitiya." Institutional Investor. Accessed May 31, 2020. Available at: https://www.institutionalinvestor.com/article/2bsx50dfm3p7vduehik8w/culture/the-unusual-ambitions-of-chamath-palihapitiya.

Palihapitiya, Chamath and Trey Lockerbie. “ Building Berkshire 2.0 with Chamath Palihapitiya” The Investor’s Podcast, 2021. https://www.theinvestorspodcast.com/episodes/building-berkshire-2-0-w-chamath-palihapitiya/.

Palihapitiya, Chamath and Oren Zeev. "Fireside Chat with Chamath Palihapitiya & Oren Zeev." ICON, 2022.

Palihapitiya, Chamath and Aqil Pasha. "A Fireside Chat with Chamath Palihapitiya w/Aqil Pasha." MIT VCPE Club, 2022.

Bryant, Adam. "Chamath Palihapitiya of Social Capital on the Paradox of Ego and Humility." 2017. Available at: https://www.nytimes.com/2017/10/20/business/corner-office-chamath-palihapitiya-social-capital.html.

Palihapitiya, Chamath and Lex Fridman. "Chamath Palihapitiya: Money, Success, Startups, Energy, Poker & Happiness." Lex Fridman Podcast, 2022. https://lexfridman.com/chamath-palihapitiya/.

Marks: The mood swings of the securities markets resemble the movement of a pendulum. Although the midpoint of its arc best describes the location of the pendulum “on average,” it actually spends very little of its time there. Instead, it is almost always swinging toward or away from the extremes of its arc. But whenever the pendulum is near either extreme, it is inevitable that it will move back toward the midpoint sooner or later. In fact, it is the movement toward an extreme itself that supplies the energy for the swing back. Investment markets follow a pendulum-like swing: • between euphoria and depression, • between celebrating positive developments and obsessing over negatives, and thus • between overpriced and underpriced. This oscillation is one of the most dependable features of the investment world, and investor psychology seems to spend much more time at the extremes than it does at a “happy medium.”

Howard Marks. The Most Important Thing (pp. 132-133). Kindle Edition.

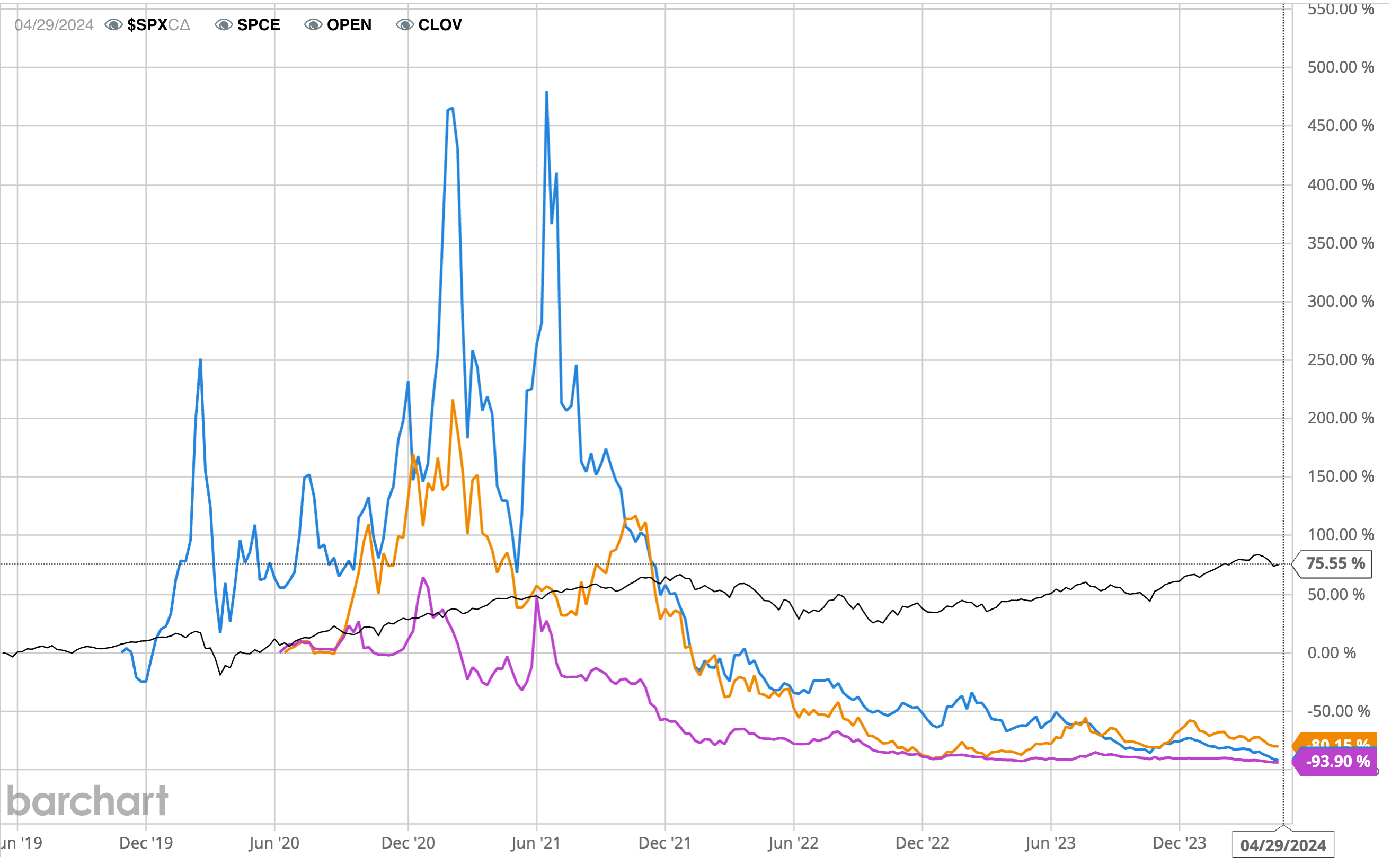

5-Year returns of S&P500, Virgin Galactic, Opendoor Technologies, and Clover Health.

In addition, see: https://www.reuters.com/markets/us/palihapitiya-wind-down-two-blank-check-firms-choppy-markets-deter-valuations-2022-09-20/

For example, see: https://www.theverge.com/2017/12/11/16761016/former-facebook-exec-ripping-apart-society

Michael Moritz: The shorter the memo, the better. I’m a big fan of the way they conduct the meetings at Amazon, without PowerPoints and with just a five- or six-page description. People tend to overcomplicate these things. For our early-stage investments we know that any financial prediction is going to be wrong, we just don’t know how wrong. So huge spreadsheets are useless and worthless. Even with the Stripe investment, which isn’t, in the grand scheme of things, that long ago, the original memo that we put together was probably no more than three or four pages. If you can express yourself clearly and you have a strong opinion, you don’t need a lot of paper.

David M. Rubenstein. How To Invest (pp. 321-322). Kindle Edition.

Marc Andreessen: We end up cooperating a lot more than we end up competing. We love competing. We really like the fight. But you end up cooperating, because it’s really up to the founders. The good founders choose their investors. They might choose us for one round. They might choose another venture firm for another round. You end up around the same table a lot of the time, working together.

David M. Rubenstein. How To Invest (p. 295). Kindle Edition.

Bezos: During our hiring meetings, we ask people to consider three questions before making a decision: Will you admire this person? If you think about the people you’ve admired in your life, they are probably people you’ve been able to learn from or take an example from. For myself, I’ve always tried hard to work only with people I admire, and I encourage folks here to be just as demanding. Life is definitely too short to do otherwise. Will this person raise the average level of effectiveness of the group they’re entering? We want to fight entropy. The bar has to continuously go up. I ask people to visualize the company five years from now. At that point, each of us should look around and say, “The standards are so high now—boy, I’m glad I got in when I did!” Along what dimension might this person be a superstar? Many people have unique skills, interests, and perspectives that enrich the work environment for all of us. It’s often something that’s not even related to their jobs.”

See: ‘Work Hard, Have Fun, Make History’ in Bezos’ 2008 Amazon Annual Shareholder Letter.